This week we’re reviewing 5 trends that have helped define 2011. So far we’ve covered online privacy, group messaging, HTML5 and second screen apps. In this final installment we’re looking at mobile payments. This has been a very busy market in 2011, as credit card companies, banks, carriers, Google, eBay and a number of startups jostle for position.

One of the defining features of the next generation of smartphones – which are starting to come out now – will be a technology called NFC (Near Field Communication). Instead of whipping out your wallet at a store, via NFC you’ll simply tap or wave your phone to make a payment. This has major implications for banking institutions and the four main payment networks in the U.S.: Visa, MasterCard, American Express and Discover. All have been actively preparing for this sea change in how we pay for things.

Over on our ReadWriteMobile channel, Sarah Perez has been running a series about the impact of NFC in 2011. Here’s her explanation of what NFC is, from the introductory post:

NFC is a newer wireless technology that allows devices to communicate with each other over short distances. The data transfer between the devices occurs through one of two means: either a short wave or, as is more common, a touch or tap.

Some notable phones available now (or very soon) that offer NFC capabilities include the Google Nexus S, as well as the Samsung Galaxy II (select models), Nokia C7, Nokia C7-00 and the Samsung Wave 578. Wikipedia maintains a list here.

Payment Processing Network Companies

All of the major credit card companies have been busy rolling out NFC initiatives.

In May, Visa announced that it will launch a next-generation digital wallet service. The platform will allow consumers to create a digitized version of their actual wallet, in which they load all their cards, whether Visa or not. Even merchant loyalty cards will be supported.

Also this year, Visa teamed up with Samsung in order to bring NFC-enabled mobile payments to the London 2012 Olympics. With any NFC-capable phone, mobile users will be able to pay for purchases using only their phone at over 60,000 locations in London.

In April, we profiled the latest from Mastercard. They’re working on SIM-based solutions, embedded solutions and the continued deployments of NFC tags.

American Express has a digital payments and commerce platform called Serve, which recently announced its first carrier deal since launching in March of this year. The company’s new partnership with U.S. operator Sprint will allow Serve’s mobile wallet application to be made available in the Sprint Zone for customers using select Android phones.

Mobile Banking

Banks are also ramping up for the mobile payments revolution.

At the end of March, we reported on a NFC mobile payments pilot program by Wells Fargo in San Francisco. The trial used Visa’s In2Pay microSD solution. There are NFC-enabled mobile wallet services under development from other U.S. banks too – including Bank of America, Chase and U.S. Bank.

Square & The Startups

As well as the banks and credit card companies, startups like Square – the mobile payment solution founded by Twitter co-founder Jack Dorsey – have been making hay in the mobile payments sun this year.

Square provides a dongle-like device that you attach to your mobile phone in order to make payments. Unlike many of the other solutions we’ve discussed in this post, Square is not powered by NFC. This year, Square got an investment from Visa. Later, in May, it announced the Square Register. The aim with that is to make real world buying as easy as a one-click Internet purchase, a la Amazon or iTunes.

As of May, Square had shipped 500,000 card readers. It did one million transactions in May, to the tune of $3 million in processing per day. The company is on track to process $1 billion in transactions within a year.

Other products to watch in this space include Card.io (you pay by holding your credit card up to the phone), Zoosh (uses ultrasound instead of NFC!), Zong (acquired by eBay in June, it’s a middleman connection between merchants and telephone companies), Payfone (which American Express invested in) and Sage (mobile payments for small businesses).

Carriers & Google

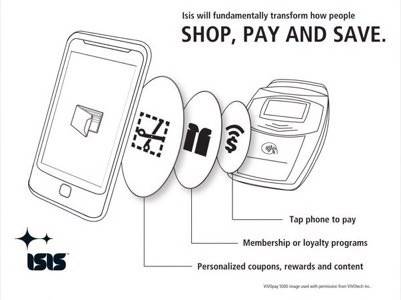

Operator-led mobile commerce initiative Isis is another mobile payments heavyweight. It has so far formed relationships with Visa, MasterCard, American Express and Discover. Isis is NFC-powered and will enable people to use their phones to pay for transactions at point-of-sale, just by tapping or waving their phone.

Finally, it wouldn’t be a web-related battle if Google wasn’t involved. Sure enough, the Google Wallet is “coming soon.”

As you can see, it’s a very busy space right now – possibly a bit too crowded. Let us know how you think it will shake out over the rest of 2011 and beyond.