NFC, or near field communication, is an emerging technology you’ll start hearing more about in the coming months. In this introductory series to understanding NFC, we’re examining the state of the industry from end-to-end, and we’ll focus on what the technology is, who’s implementing NFC-enabled solutions and how those solutions will work.

One of the future use cases for NFC is to create a “mobile wallet” of sorts – a comprehensive service that houses everything from bank cards to coupons, all managed, accessed and delivered via your mobile phone. But what companies are building mobile wallet solutions today and whose mobile wallet will you use?

This is the second post in a series on NFC here on ReadWriteMobile which will serve to get you up to speed on what NFC is, what notable developments are underway and what commercial programs using NFC will arrive this year. You can follow this series by clicking the tag (or bookmarking the tag) “NFC 2011.”

Before we could begin talking about NFC developments, advances and upcoming commercial programs in specific, we first had to get you up to speed with what exactly NFC is. The first post in the series is the best starting point for those unfamiliar with the technology. In the post below, we’ll examine the different types of mobile wallet initiatives that will use NFC.

How Can a Phone Replace a Wallet?

When you think about a technology designed to replace your actual wallet – you know, the beat up leather-bound bill holder containing cash, credit and debit cards, paper receipts, coupons and discount cards – you begin to realize what a complex undertaking it is for any one company to deliver a complete solution.

A credit card company like Visa may team up with your bank to offer you a way to use your mobile phone as a replacement for a single plastic credit card, but it’s only one piece of the pie. What about the coupons? What about your loyalty cards? What about the rest of your credit and debit cards from other banks?

At present, Apple, Google and other mobile platform providers are likely working on a comprehensive mobile wallet solution for consumers, but they lack experience in some areas where financial services companies excel: providing customer support for issues like the proper handling of chargebacks, understanding the relevant regulations that apply to the industry, implementing the necessary level of security that must be involved when processing transactions from a host of merchants and hundreds of thousands of customers through a large worldwide network built for transactions, and other concerns.

Given these challenges, it’s not a sure thing that your preferred mobile wallet provider will be the one Google or Apple or another mobile platform provider creates; it may be a service from your mobile carrier (for example, here in the U.S., Verizon, Sprint, T-Mobile or AT&T).

A third possibility is that your bank itself ships some type of complete mobile wallet system as a part of their mobile banking/mobile payments product. In this mobile wallet, other third-party services could complement the bank-provided, NFC-enabled debit and credit “cards” you use on your NFC-enabled mobile phone. (Not actual plastic credit cards, but digital ones, stored on your device).

There’s no real answer to the question about who will be the dominant mobile wallet provider, not only because these services have not yet launched (or are just now doing so) but because when they inevitably do, there’s no way to foretell which service consumers will actually prefer.

To begin our overview of mobile wallet, we’re going to look at three different types of players, which we will break down into three categories we’ll call the apps vs. the operators vs. the banks. But first, let’s examine what a mobile wallet actually is.

But What Is a Mobile Wallet?

A mobile wallet, or an e-wallet (or in Apple’s case, an iWallet!), is not just a smartphone application that you download from an app store. To the end user, there may be an icon on their homescreen that launches the user interface to your mobile wallet, but that is only a part of the overall solution. The complete mobile wallet solution actually consists of both the user interface itself and the secure element chip on the phone where your personal data (your credit card number, passport ID, shopping history, coupons, etc.) is stored. The user interface allows you to interact with NFC applications and with the secure data stored on the secure element on your device. A third part of the solution is the antenna, which is the piece that makes the near field communication possible.

It’s the secure element on the phone that’s the most important part to the mobile wallet, though, and it’s why the wallet isn’t just “another app.” Sarah Clark, an editor for NFC industry trade publication NFC World, describes the secure element like so: “[It] acts like an electronic version of your wallet and can be used to replace everything from credit cards and loyalty cards to bus and train tickets, library cards, door keys, coupons and even cash.”

This secure chip, she explains, “can be built into mobile phones and other devices by the manufacturer, they can be integrated into SIM cards issued by mobile networks to their subscribers and they can be added to existing phones via special microSD cards or stickers issued by banks and other organizations.”

Your mobile wallet will likely arrive empty, she says, just like a regular wallet does. You will fill it with whatever services you want.

1. Mobile Wallet Solutions from Mobile Platform Providers (Apple, Google, Etc.)

When we talk about mobile wallet “apps” from the mobile platform providers, you now understand that what we mean is an app that serves as the interface to a comprehensive mobile wallet solution where all your bank cards, bank accounts, coupons, loyalty cards, receipts and more are duplicated on your phone. These simply don’t exist yet here in the U.S.

There are so-called “mobile wallet solutions” of a sort today – but not the kind that will exist in the future. For example, U.S. carrier Sprint introduced its Sprint Mobile Wallet back in October 2010. But this initiative is designed for online purchases, not purchases of physical goods in the real world where a tap of your phone at checkout deducts the payment from your personal bank account.

It’s expected that the mobile platform providers are building more complete mobile wallet solutions that use NFC, however. Google introduced support for NFC technology into its Android mobile operating system (version 2.3, aka “Gingerbread”) and it recently pushed out an update that makes that function work both ways – read and write – a necessary component to any mobile payments system.

More on Google’s NFC plans: Google Considering a Mobile Payments Service, January 2011

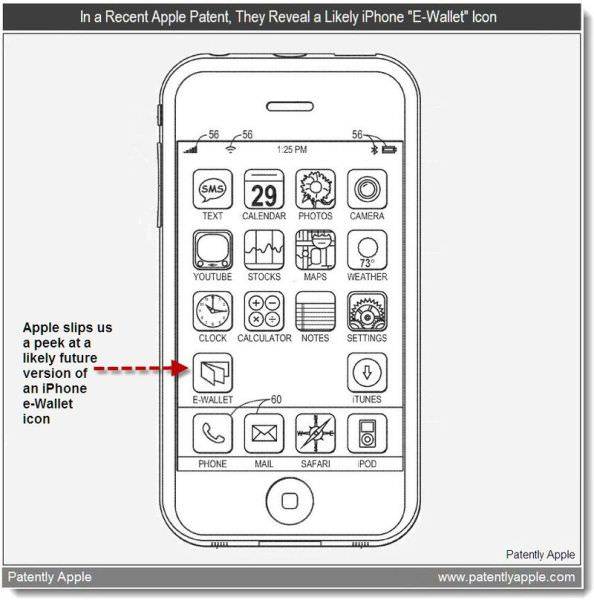

Apple, too, has various NFC-related patents on file and has hired a well-known expert in the field, but, as usual, is completely silent on what it has in development. We can only speculate what the company is working on by tracking its patent applications – like this one spotted in February 2011 which shows an e-wallet icon. The general expectation is that Apple’s e-wallet will work with the NFC technology built into a future iPhone.

Although few would ever bet against Apple, it’s still fair to say that implementing NFC and financial services for a mobile wallet solution of this scale requires significant investment and, frankly, a massive amount of work. Even a company as accomplished as Apple will find that to be complex challenge.

In addition, what the mobile platform solutions also have to deal with is how to handle – or ignore – the mobile carriers’ desire to be involved. While Apple has traditionally proved itself to be a company whose goal is to disrupt the control a carrier has over the handset, successful NFC solutions in other parts of the world have always had operator involvement. In fact, they’ve typically been joint programs launched via a partnership between banks and operators alongside support from handset manufacturers, not cases where a single player like Apple tries to go it alone. Of course, this is Apple. It could be the one to buck that trend.

2. Operator-Provided Mobile Wallets

Speaking of operators, lets make this clear: they want to be involved. Not only that, but they want to be the mobile wallet providers. To that end, they’ve teamed up to make sure that happens.

During February’s Mobile World Congress in Barcelona, some of the world’s largest mobile operators announced their intentions to launch commercial NFC services. In total, 16 operators – América Móvil, Axiata Group Berhad, Bharti, China Unicom, Deutsche Telekom, KT Corporation, MTS, Orange, Qtel Group, SK Telecom, SoftBank Mobile, Telecom Italia, Telefónica, Telekom Austria Group, Telenor and Vodafone – declared their support for the technology. For these operators, NFC isn’t just about the mobile wallet. It can also deliver services like mobile ticketing, mobile couponing, information exchange and the ability to control access to things like cars, homes, offices, hotels and more.

In the mobile operators’ case, the deployment of NFC would involve using the SIM card in the phones as the secure element that provides the necessary authentication, security and portability.

As NFC World notes, Apple’s and Google’s initiatives will be based on embedded secure elements within the phones themselves – such as the technology found today in Google’s latest flagship phone, the Nexus S – not the SIM card. To some industry watchers, the teaming up occurring now among mobile operators on the matter of NFC is a clear confirmation that the next iPhone (the iPhone 5), will almost certainly have NFC built in.

In addition to the GSMA announcement, three of the four major mobile operators in the U.S. (Verizon, T-Mobile and AT&T) have joined forces to launch Isis, a mobile payments venture that will use Discover Financial Services’ network to process payments. Barclaycard U.S. will be the first to issue customers Isis accounts. This mobile wallet solution will handle both credit, debit and prepaid transactions. It’s expected that Barclaycard will be the first of many card issuers to come on board with the venture.

More on Isis: AT&T, Verizon, T-Mobile Join Forces in New Mobile Payments Venture Called “Isis”, November 2010

Isis claims that it already has recruited some merchants to use its service, but will not name names just yet. The group knows that getting merchants to adopt the technology is critical. Merchants don’t want an AT&T-only solution, Jim Stapleton, head of sales and account management at Isis and a veteran of AT&T Inc., told the website Digital Transactions in February 2011.

Operators know that to force consumer adoption of a new technology, it must be integrated into their daily lives on a regular basis. That’s why Isis is first talking to merchants at coffee shops, grocery stores, quick-service restaurants, parking lots and garages and most importantly, transit systems (bus, train, subway, etc.). Getting these types of merchants on board with the initiative is critical for its success.

Meanwhile, on the consumer side, Isis wants to offer more than just payments. It also wants to also offer electronic coupons, loyalty programs and ticketing, reports Digital Transactions, referencing a statement made by Sarab Sokhey, a Verizon Wireless non-payment NFC executive and advisor to Isis.

3. Banks and Mobile Wallets

A third category, and one not necessarily mutually exclusive to categories number one and two above, is the one that involves banks. While a bank card may be integrated at some point into a complete mobile wallet solution, such as the one offered by Google or Apple or your carrier, for now, some banks are forging out on their own with NFC-enabled mobile banking products. We could also consider these “mobile wallet services,” of a sort.

On this front, there are NFC-enabled mobile wallet services under development now from several U.S. banks including Bank of America, Wells Fargo, Chase and U.S. Bank. All four banks have trials underway in major cities using Visa’s In2Pay microSD solution, for example. This solution became commercially available from Visa back in December 2010, but it needs the banks’ involvement to really take off in the consumer space.

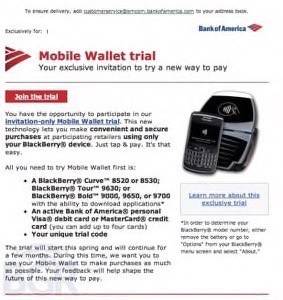

Bank of America’s mobile wallet program, which will launch in the second half of this year, recently made the news when the blog BGR spotted an invitation the bank was sending customers to try the BlackBerry microSD solution (a microSD card with NFC capabilities). Visa told us that Bank of America was already testing this solution in major markets including New York, San Francisco and L.A.

The microSD technology Visa uses is provided by a company called DeviceFidelity, which also makes solutions for iPhones and Android devices. The microSD card is inserted into a phone’s memory slot, when possible, to NFC-enable the device. But in the case of the iPhone, a slot is not available. DeviceFidelity works around this issue by using a special, protective case for iPhone users where its microSD functionality is built in.

It should be noted that these sorts of microSD and case solutions are a way to NFC-enable both current and older devices where NFC is not built into the phone itself. In the future, as NFC technology becomes more prevalent, such a solution would not be required.

While they’re more of the dark horse in the race to become complete mobile wallet provider, it’s possible that banks could expand their mobile wallet solutions to include more than just the NFC-enabled credit card replacement technology, but could expand their programs by integrating solutions from third-party providers. But for now, banks are solely focused on replacing just your payment cards (debit, credit and prepaid). For some consumers, that may be enough for now.

In future posts in this series, we’ll look at some of the solutions mentioned above in more detail. Stay tuned.