Isis, the NFC-enabled mobile payments venture led by three of the top four U.S. mobile operators, Verizon, AT&T and T-Mobile, is accelerating and broadening the scope of its offering, not scaling back, as The Wall St. Journal recently reported. This is according to Jaymee Johnson, Isis’ Marketing head, who also says that the group was “very displeased” with WSJ’s article, which he called “massively misleading.” But the Journal had picked up on something going on within Isis: change.

Instead of going to market with one issuer and one payment network, as originally planned, Isis is planning to partner with multiple issuers and networks, Johnson explains.

This article is part of a series on NFC here on ReadWriteMobile which will serve to get you up to speed on what NFC is, what notable developments are underway and what commercial programs using NFC will arrive this year. You can follow this series by clicking the tag (or bookmarking the tag) “NFC 2011.”

This post assumes you are familiar with the term NFC as well as the technology’s use in the mobile industry. If you’re just starting to learn about NFC, you should begin here with the first article in the series to get caught up.

What’s Isis?

Originally, the operator-led Isis initiative planned to launch with Discover and Barclays U.S., but now the company will launch with multiple payment networks and banks when it goes live in 2012. Which ones will be on board at launch? Johnson can’t say, but notes that it’s now open to all comers. And by “all,” Isis doesn’t just mean all banks, it means any other mobile operators, card issuers, Apple, Google or anyone else who wants in.

It’s a big change and a bold move for Isis, especially in light of the recent news that Google is moving forward with its own NFC plans, due to be announced later this week. But it certainly makes more sense for Isis to try work with others in the same space, instead of trying to go it alone with its own payments network.

Johnson says the new iteration of the service will work like “connective tissue” to bring the payments, mobile and retail industries together, all of which need be be involved for NFC to work. Isis thinks it has a good shot at success because payments is “ultimately a scale game.” There’s a logistical problem getting payments to work across dozens of handsets, running multiple versions of multiple mobile operating systems on multiple mobile networks, Johnson explains. Isis wants to help move NFC-enabled payments out of the fragmentation game, and into scale.

How Will Consumers Use Isis?

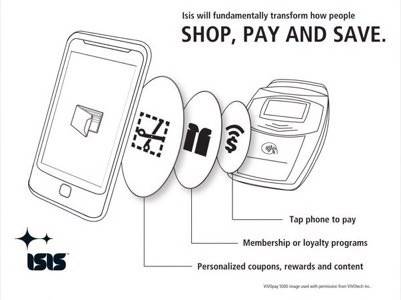

For consumers, the appeal of a mobilized, digital wallet is not hard to grasp. Instead of carting around a physical wallet with dozens of credit, debit and store loyalty cards, you would only need your phone. To make a transaction, you would just tap or wave your phone at the contactless NFC reader at the point of sale. If you also had a loyalty card with that store (and you likely do: U.S. consumers have, on average, 12 to 15 of these), that transaction could automatically apply discounts, deliver new coupons or other offers or rewards upon checkout.

On consumers’ phones, the Isis mobile app would run in the background, ready for use at any time. For security-minded shoppers, an additional, optional feature will be available that prompts users for a passcode to access the Isis wallet.

In addition, through developer tools like APIs (application programming interfaces), consumers could virtually “clip” coupons from a variety of sources – not just those sent directly from the merchants themselves to the device. These other coupons could come from manufacturers’ websites, online couponing sites or even physical marketing materials like in-store ads, posters, and more, all of which could be NFC-enabled. The coupons, once loaded into the wallet, could be used at any participating merchant, just like their offline counterparts are.

Johnson admits that there will be a need to build up awareness at first about NFC, mobile payments and what the technology can do. However, from early trials and research, the industry has found that once the consumer interacts with the technology, the behavior is quickly and easily adopted, he says. To build up mainstream awareness, Isis plans to run ad campaigns, TV commercials and will have marketing materials in carriers’ stores, explaining which phones are “payments capable” and what that means.

What Isis Will Offer Merchants

For merchants, NFC and mobile payments offer them an avenue to get onto the mobile phone. Through opt-in relationships with consumers, retailers can open a dialog with customers, track their shopping trends and then send out targeted offers through various mobile merchandising channels.

Isis says it will provide a toolset to merchants that will enable them to communicate specific offers to specific customers, like those based on your past shopping trends, demographics or physical location. It will also offer merchants NFC-enabled product tags for store shelves, and a backend to program those tags with additional information. That way, a customer could tap the tag to get product details or even a coupon.

This technology could aid shoppers at large, warehouse clubs, where customer service out on the floor is rarely available, but it could also appeal to discount shoppers who today grab a coupons from the holders (like “blinkies“) on grocery store aisles for an immediate discount. With Isis, they would just have to tap their tap to receive the same deal, no paper coupon required.

Where and When Will Isis Launch?

Isis plans to launch first in Salt Lake City, Utah in 2012, the company says. It may seem like an odd choice for the first market, but Johnson says that the city is actually an ideal testing ground for NFC mobile payments. The entire public transit system there is already contactless-enabled, whereas in other NFC testbeds, like New York City for example, contactless is only available on one or two lines of the transit system.

In addition, Salt Lake City’s population is educated, innovative and receptive to business, which makes it a good market for testing. And the city is the only major population center for hundreds of miles, which gives Isis a “clean read” on what adoption trends are like in an urban market.

In a matter of weeks, Isis will be announcing its second market, but cannot reveal the location at this time. It will then continue to launch in additional markets through some sort of logistical sequence, for example, moving north to south throughout a given geographical region.

Revenue Generation

One of Isis’ main offerings is its platform for secure provisioning which enables banks and other card providers to mobilize their existing card relationships. The card issuer may not know the phone’s maker and model, its software, the customer’s operator or where on the phone the secure element is located (where the card information is stored). To aid the issuers, Isis will handle the provisioning for a fee, which will be a source of revenue for the company.

It will also charge merchants for the use of its offer-delivering engine which allows retailers to track offers all the way through redemption. Just like online advertising enabled a new business to spring up around cost-per-click, cost-per-impression and cost-per-action type ads, mobile advertising will enable its own form of opportunities, but though a more cost-effective, targeted channel, the company believes.

Will Isis be successful? It’s far too soon to tell. But the only major concern the company has at this time are the new federal regulations around debit cards, as proposed by the Dodd-Frank financial reform law. The regulations make payment processing less profitable by reducing fees merchants pay for customers using debit cards. That means that merchants will continue to take Visa and MasterCard payments, and have less incentive to work with new payment and commerce systems, such as the one Isis originally planned using Discover’s smaller payments network. This is one of the reasons why Isis had to change its course, and open up to working with more players, as detailed above.

Now, Isis says it still hopes to work with its original partner Discover, but Johnson could not confirm whether or not it would be on board at launch. Although Isis isn’t launching in 2011, you should expect to hear more from the group in the coming months.