The term “mobile payments” has been around for several years now. Really though, who knows what it actually means?

Different aspects of the payments industry want you to think different things. PayPal wants you to think of mobile payments as when you pay for something on your smartphone through an app or a website. Startups like Square think more along the lines of location-based payments, where you actually use your smartphone to process the transactions. Then there is the ability to transfer funds, pay bills or bank with your smartphones. To the payment processing sector, they all fall under the notion of “mobile payments.”

By this logic, PayPal can claim that it is one of the biggest mobile payment processors in the land, when really, it has next to zero physical infrastructure in existing retail environments. It is looking to change that with its recent NCR deal, but it will take time for the payment processor to create the necessary infrastructure. When PayPal touts its mobile payment numbers, what it is really saying is that it is the transactional arm of mobile commerce – mCommerce – the fledgling little brother to eCommerce, popularized on the Web by Amazon more than a decade ago.

3 Kinds Of Mobile Payments

In a new report, research firm Forrester has broken down the definition of mobile payments into three categories:

- Mobile proximity payments: In-store or location-based payments with a smartphone to a point of sale. This could include a taxi driver using Square, a burger joint using LevelUp or a gas station using Near Field Communications (NFC) and a payment processor like Google Wallet.

- Peer-to-peer payments and remittances: Sending money between two people through a mobile device.

- Mobile remote commerce: Buying an item (digital or physical) through a mobile device from an online retailer.

Forrester’s broad definition of mobile payments is, “a transaction in which the transfer of funds is initiated using a mobile phone – excluding the ‘voice’ function of the device.”

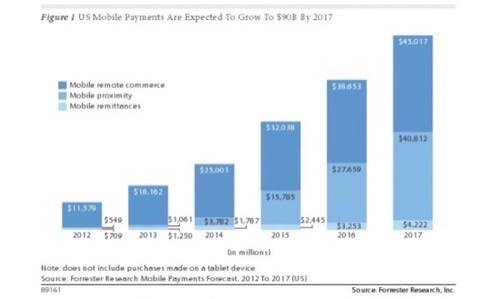

When the media talks about mobile payments, it is almost exclusively talking about proximity payments, usually tied to the potential (or lack thereof) of NFC. Mobile commerce is something completely different from actual mobile payments. In 2012, more than 90% of mobile payments (as defined by Forrester) were mCommerce related.

Forrester notes that mobile payments will reach $90 billion by 2017, a compound annual growth rate of 48% from the $12.8 billion in 2012. Of that $12.8 billion, only 4% were proximity payments ($549 million). Forrester predicts that by 2017 that mCommerce will drop from its current rate of 90% of the overall mobile payments industry to 50% while proximity payments will grow to 45% of the toal ($40.8 billion).

Getting More Realistic

Forrester’s predictions are more realistic than what we have seen from other research groups. Juniper Research had predicted that mobile payments would be a $670 billion industry by 2015. Granted, Juniper’s prediction took into account other aspects of the payment industry on a global scale, such as direct-to-carrier billing and mobile bill pay along with proximity payments and remote mobile commerce. Still, Juniper predicted exponential growth that was completely unrealistic given the limitations of building mobile payment infrastructure and the chicken-or-egg nature of the digitization of mobile payments.

When it comes to proximity payments, Forrester notes the standoff between consumers and retailers when it comes to setting up point-of-sale services to pay via smartphone. Consumers do not care to make mobile payments until a significant portion of retailers have the capability – while retailers do not want to set up the capability until a proven number of consumers are willing to pay via their phones. As such, 2013 will be the proving ground for mobile payments with many pilot programs being tested by payment vendors and retailers before true growth starts to ramp up in 2014.

How Much Extra Would You Pay?

Seth Priebatsch, founder of mobile payments startup LevelUp, told me once that he would pay an extra 10% just to pay with his smartphone because, essentially, he thought it was cool. Most (heck, all) consumers are not likely to share that sentiment. Forrester notes three directives that will need to occur for proximity payments to begin accelerating:

- Increased benefit and convenience

- The ability for payment systems to scale among retail bases

- Reduced barrier to entry for early adopters.

Essentially, it should be really easy to pay with your phone and it should be good for you and the merchant.

Cash, plastic cards, checks and other forms of payment are not going away any time soon (well, checks may be on the way out). According to Forrester’s predictions, despite mCommerce and proximity payment rates, mobile payments will be only a drop in the bucket of the overall transaction landscape.

If you were hoping that a mobile-payment-driven cashless utopia would arrive by the end of the decade, you might want to start dreaming about something else.

Top image courtesy Shutterstock.