For a technology startup company to launch an initial product and survive long enough to gauge its success, requires two-orders-of-magnitude less money today than at the start of the previous decade. This from a man who knows from having made bigger investments that are smaller: Duncan Davidson, Managing Director of Menlo Park-based Bullpen Capital.

Bullpen is one of a growing number of early-stage funds – or, perhaps more accurately, “earlier-stage,” since even his is no longer the first out of the gate. In an interview with ReadWriteWeb, Davidson explains how the latest industry to receive the disruption treatment has been the venture capital business itself, with the epicenter of the quake right around San Francisco.

For more of Duncan Davidson’s insights – along with those of five other top-tier VCs – download Scott Fulton’s exclusive 14-page report: “Growing Your Business In The Modern Economy: 6 VCs Weigh In.”

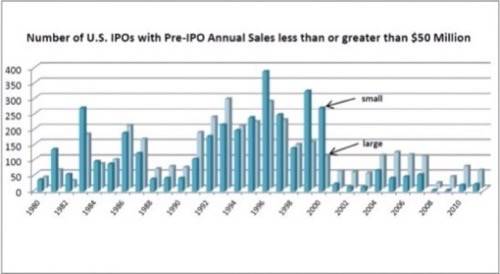

“There used to be the Four Horsemen of the IPO world, back in the ’80s and ’90s. They were some great, small banks: Robertson Stephens, Hambrecht & Quist, Alex. Brown & Sons, Montgomery Securities. They all went away; they got rolled up in 1999 and 2000 into these too-big-to-fail banking operations,” Davidson tells us. “The question is why? The answer is, they couldn’t make any money trading, [or on] giving analyst support for small stocks because the spread got too small.”

The spread he’s talking about is the decimalization of the U.S. stock market: The change led by NASDAQ in early 2001 to valuing stocks in increments from one-eighth of a dollar down to one cent. “When you make the spread a penny, only very high-volume stocks can garner economic value for the banks to be worried about it,” says Davidson. Firms that gave analyst support for small stock issues used to provide price target projections that had some meat between the bones because their highs and lows were separated by eighths of a point.

Believe it or not, this is where the change begins. When small fluctuations in stock value changed from 12.5¢ down to 1¢, the meaning of small stock got smaller. Decimalization forced analysts to tighten their spreads, the result being that their analysis looked like they were wasting their time commenting on penny stocks. It became unprofitable for the Four Horsemen to continue doing business independently. When they exited the scene, the small IPO market followed suit.

What followed is what the VC industry now calls “The Era of Cheap,” and we’re still very much in it.

Number of U.S. IPOs by year, 1980-2011, with pre-IPO last 12-month sales less than (small firms) or greater than (large firms) $50 million (2009 purchasing power). Credit: Professor Jay Ritter, for testimony before the Senate Banking Committee

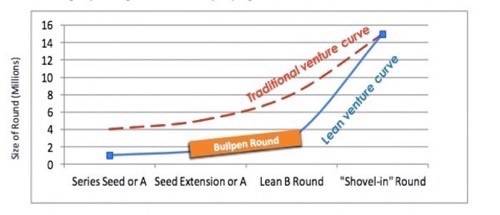

The way startup funding worked at the turn of the decade, he describes, small firms would raise “seed round” capital from friends and family to get off the ground. From there, they’d make the leap to “Series A,” which used to refer to the first round of institutional capital invested. Davidson says, “Those are the funds you’ve all heard about: Sequoia, Kleiner Perkins, Mayfield and a whole bunch of great funds. The reason you had to do that back then was because it took $5 million to launch a company into the marketplace, or at least to get the technology done and see [how it performed].

“What’s happened in the last decade, the cost of launching an Internet product – forget other technologies, we’ll focus on Internet – has dropped from $5 million to $500,000 in 2005, to $50,000 today,” he continues. “Two orders of magnitude. That’s why a couple of kids in their dorm room can start a company, launch it, and see if anybody cares out there. With that great decrease in cost to launch something, you have the emergence of all these new funds. The emergence has been extraordinarily traumatic and disruptive on the venture industry.”

By Bullpen’s count, at least 80 new firms have been formed recently with the intention of helping newer firms raise smaller amounts prior to what’s still called the “Series A” round, though it may have become the fourth or even fifth rung on the totem pole.

A startup (or what the newly passed JOBS Act calls emerging growth companies, or EGCs) may not need a seven-digit investment until what’s called the “seed round,” but what’s really round three after the “accelerator round.” Bullpen may come into play with about $2.25 million on average, before “Series A” even begins.

“It’s all driven by the Era of Cheap,” says Davidson. “It’s all because it’s a lot less expensive to start a company than it used to be, so you keep the amount of funding in much, much less, and as long as you can before you go for big money.”

Davidson’s company explains that backers are looking for companies that can sustain leaner growth models. It’s still growth, mind you, but it’s more efficient, less wasteful, and a bit less self-assured. A company can validate its growth metrics, Bullpen believes, in as little as four to six months after its initial funding periods.

“You don’t know if these deals are real; it’s all an experiment. And the leaner you keep it, the more options you have with what to do with it. Once you put a lot of money in, you’re no longer lean and flexible and kinkin’ and jivin’ and trying to figure it out,” he says. “Now you’re on a bit of a race to actually prove out the value of the money you raise, and scale it. When you keep it lean, everybody has better options, and a better outcome when all the dust settles.”

The benefit for Bullpen, and other investors in its space, is risk avoidance. Having a little less money to burn drives the EGC to get its product to market on time. Then the risk of that product succeeding is lessened by network effects made feasible by app stores and digital distribution, driving up customer adoption. Risk to the company’s business model in the early stages is reduced by adopting this app store “template” that customers worldwide have already embraced.

“Look at Instagram, which got bought by Facebook. How old is Instagram? It’s not a very old company, and it just sold for a billion dollars. Zynga goes from zero to multi-billion-dollar company in four years. There’s been two fundamental changes here that have been overlooked by a lot of people, and this is why it’s fundamentally different than it was in 1999: One change is this Era of Cheap and the lean finance model… Everything’s better with the lean model.

“Money, in effect, can be a drug – it can be a problem,” he continues. “You get too much money, you lose flexibility instead of gaining it. You pay yourself too much money, you sort of relax, you don’t have the same urgency – all these things happen when you take too much money in. In a lean model, you’re in a race, you’re worried, you’re not there yet. You’re at a constant level of anxiety, and it makes you more agile and responsive – a lot of good things happen.”

The second change comes from the globalization of technology markets made possible by the Internet, as Bullpen’s Duncan Davidson explains: “You’re not just selling to a few companies in the U.S.; you’re selling to a huge consumer marketplace. So a franchise can evolve extraordinarily quickly. Bill Gates once called this the ‘friction-free economy,’ and it’s pretty damn close. This explains why a company like Zynga or Groupon or Instagram can go from nowhere to a very valuable company, extraordinarily quickly, much more rapidly than ever before. The changes are: It’s very cheap to do things, given modern technologies, and the global market makes a potential win absolutely huge – faster, bigger than we ever imagined before.”

(NOTE: For more of Duncan Davidson’s insights – along with those of five other top-tier VCs – download Scott Fulton’s exclusive 14-page report: “Growing Your Business In The Modern Economy: 6 VCs Weigh In.”)